Environmental Risk Intelligence Is Not Just for Governments

When people think about flood, wildfire, seismic, or drought risk, they usually think about public authorities. Civil protection, emergency agencies, municipal planners, technical teams with specialized tools and dedicated staff.

That view is understandable. But it is incomplete.

Environmental risk is not just a public-sector issue. It is a business issue. And for many organizations, it is becoming a strategic one.

If a company has branches, stores, insured properties, substations, warehouses, supplier networks, financed collateral, field teams, or customers distributed across territory, then environmental risk is already part of its reality - whether the company is managing it properly or not.

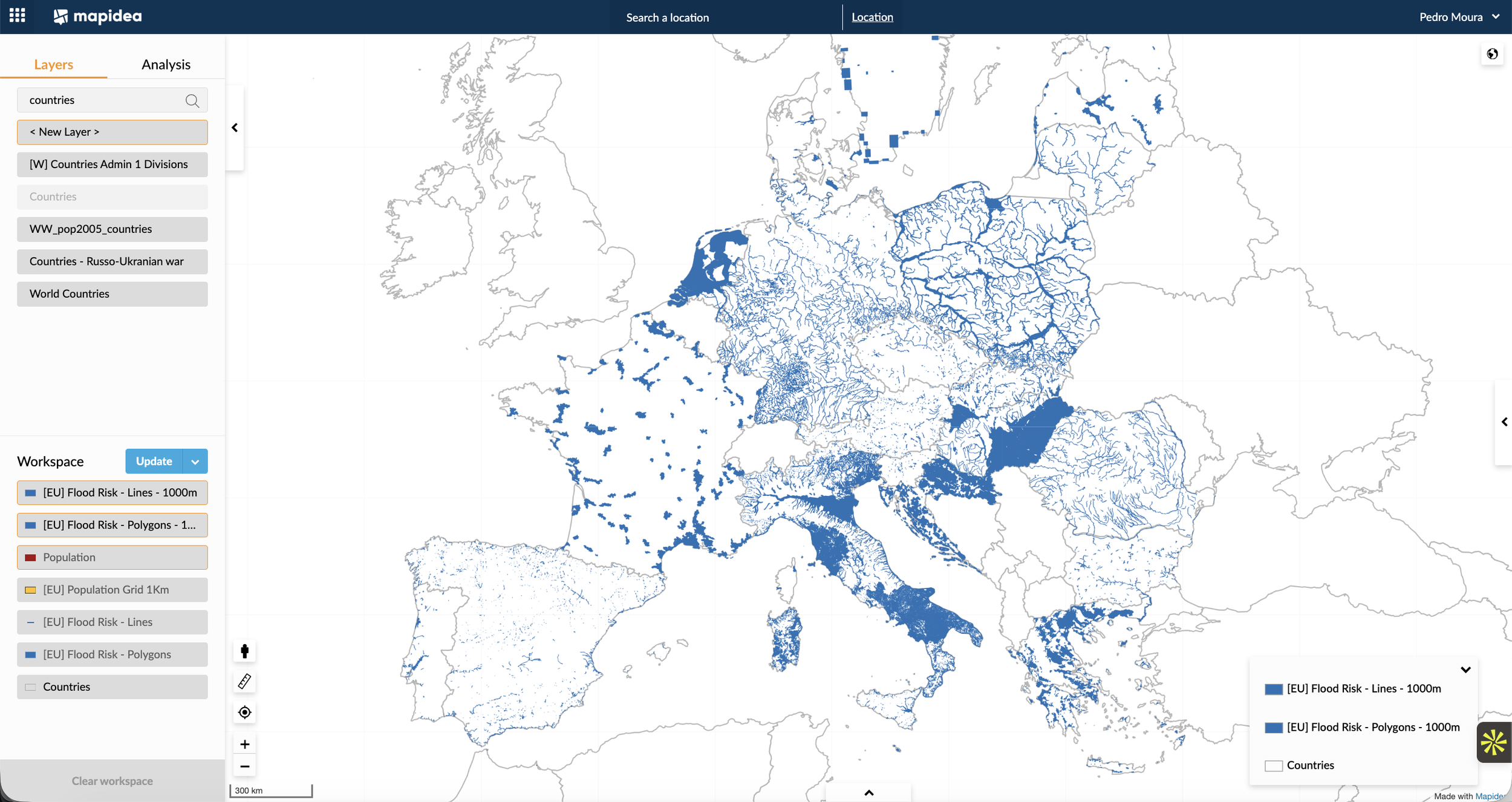

A European view is enough to make the point

A simple European map of flood risk areas already changes the conversation. Risk is not confined to a few exceptional places. It is distributed across territory at scale, crossing borders, administrative divisions, and business footprints.

That matters because most private organizations do not operate in just one point. They operate across networks - branch networks, insured portfolios, utility assets, supplier bases, service territories, logistics routes, or store footprints. Once risk is seen at that scale, it stops looking like a technical footnote and starts looking like a management issue.

And floods are only one example. The same logic applies to wildfire, seismic risk, landslides, drought, coastal hazards, and other geographically uneven threats.

This is already a business issue, whether companies admit it or not

A surprising number of organizations still behave as if environmental risk is someone else’s problem. It is not.

For insurers, it directly affects underwriting quality, accumulation control, claims exposure, and post-event response.

For banks, it affects mortgage collateral, commercial real estate portfolios, branch resilience, and climate-related risk assessment.

For utilities, it affects substations, overhead networks, field operations, vegetation management, and service continuity. For telecom operators, it affects towers, routes, maintenance access, and network resilience.

Retail and logistics are no exception. A flood-prone store is not just a property problem - it can disrupt revenue, staffing, inventory, deliveries, and customer access. For logistics operators, warehouses, depots, transport corridors, ports, and last-mile routes all carry territorial exposure. For real estate players, environmental risk should influence acquisition screening, due diligence, insurance strategy, and portfolio monitoring.

For manufacturing, the issue goes beyond the plant itself to include supplier locations, workforce access, infrastructure dependency, and continuity of operations.

Healthcare, pharma, hospitality, tourism, data centers, energy, and construction all face similar realities in different forms. Once a business depends on geography, environmental risk becomes part of management, not just compliance.

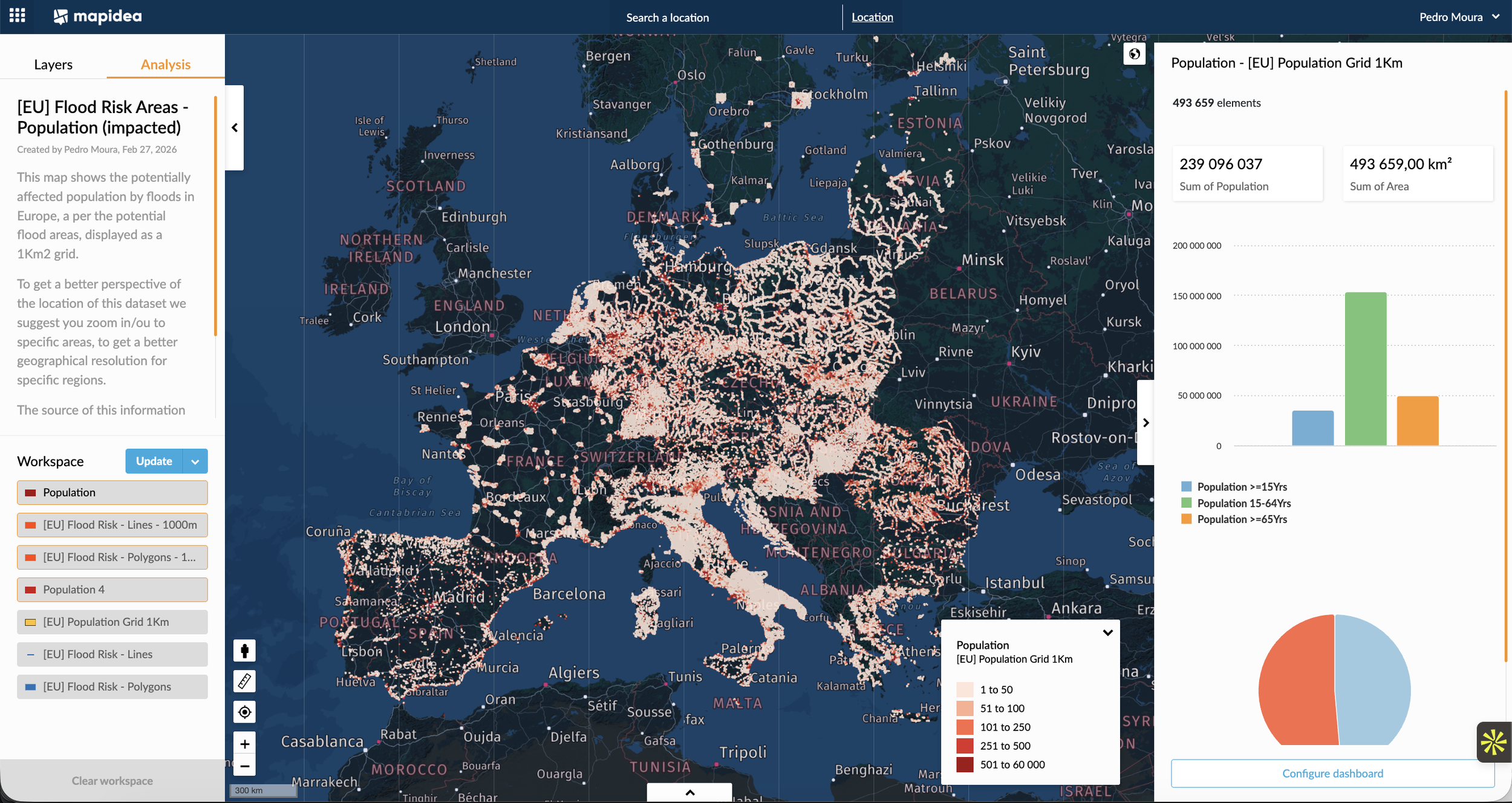

A second image makes the issue impossible to ignore

A map of the population potentially affected by floods pushes the discussion further. It is no longer only about hazard zones. It becomes about people, customers, households, service demand, and operational exposure.

This matters across industries in very practical ways. An insurer sees potential claims exposure. A bank sees households behind mortgage portfolios. A retailer sees catchments and customer demand at risk of disruption. A utility sees service areas and vulnerable populations. A telecom operator sees where outages may affect large concentrations of users. The same layer means different things to different businesses, but in all cases it becomes more actionable when viewed through the lens of the organization’s own footprint.

Access to data is not the same as operational capability

This is where many organizations still fall short. A lot of environmental risk data is already accessible in online viewers, simple visualization tools, or downloadable files. That is useful. But it is far from sufficient.

Seeing a flood layer on a map is not the same as using it operationally. The real challenge is being able to access that data easily, blend it with the organization’s own assets, branches, stores, insured properties, substations, loan collateral, customer concentrations, supplier sites, territories, and service routes, and then give business users simple ways to analyze it without depending on a small technical elite every time a question arises. That is fundamental.

A flood map by itself says, "this area may be exposed." A flood map combined with business data says, "these are the assets, customers, operations, and decisions that are exposed."

That is the difference between data availability and decision capability.

The real value appears at the local level

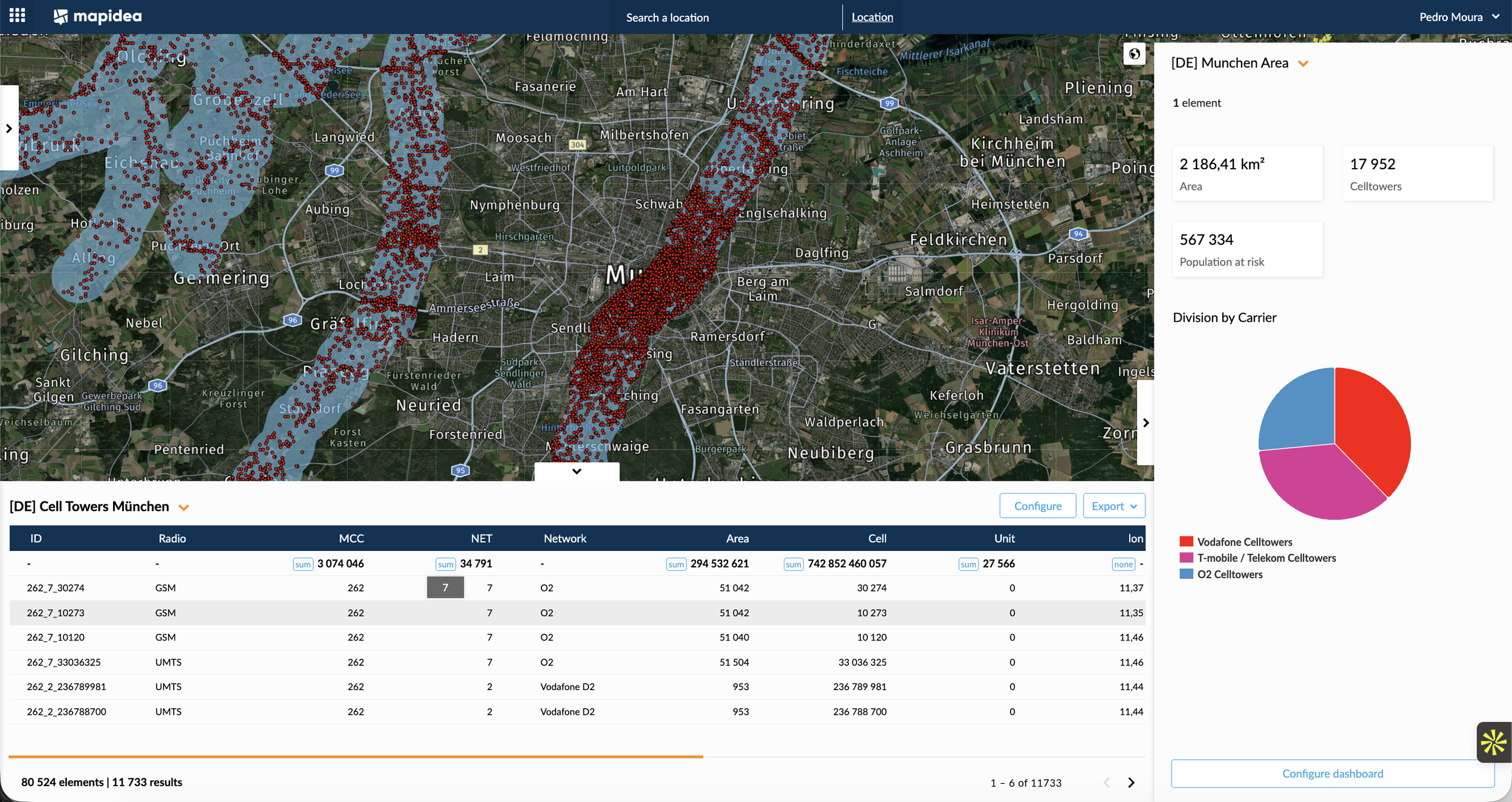

This becomes even clearer when analysis moves from continental scale to operational scale.

Looking at cell towers within flood risk areas in and around Munich makes the issue immediately more concrete. At that level, environmental risk intelligence stops being a general awareness exercise and becomes a business tool. A telecom operator can identify which assets are exposed, where service continuity may be at risk, which intervention priorities make sense, and where mitigation or contingency planning should be strengthened first.

And this logic is not limited to telecom. The same type of analysis can be applied to bank branches, insured properties, substations, warehouses, stores, clinics, logistics depots, or financed real estate assets. Once hazard layers are combined with business assets, organizations can move from “where is the risk?” to “what exactly is exposed, and what should we do about it?”

This is where geospatial intelligence becomes genuinely useful to the business. Not as a static map in a report, but as a working environment where environmental risk data and company data can be combined, explored, and used by business teams.

That shift matters. It allows organizations to screen new locations before investment, monitor portfolio exposure, identify concentrations of risk, support underwriting or credit decisions, prioritize mitigation measures, prepare field operations before events, and strengthen continuity planning with actual spatial evidence.

Final thought

Environmental risk intelligence should not be treated as a specialist luxury reserved for governments or technical agencies. It should be treated as a business capability, easily accessible to regular business users, not only geographic intelligence specialists.

Floods, fires, seismic events, drought, and other hazards do not care whether the exposed asset belongs to a public authority, an insurer, a bank, a retailer, a utility, or a logistics operator. They affect whoever is exposed.

The organizations that can combine environmental risk data with their own business data, and make that intelligence accessible to business users, will be better prepared to protect assets, improve decisions, and reduce avoidable surprises. The rest will keep discovering, too late, that geography was never just background.